Free Preparation Discussions

CFA Institute CFA-Level-II Exam Questions

- Topic 1: Equity Valuation

- Topic 2: Financial Reporting and Analysis

- Topic 3: Ethical and Professional Standards .

Free CFA Institute CFA-Level-II Exam Actual Questions

Note: Premium Questions for CFA-Level-II were last updated On Mar. 06, 2026 (see below)

Delicious Candy Company (Delicious) is a leading manufacturer and distributor of quality confectionery products throughout Europe and Mexico. Delicious is a publicly-traded firm located in Italy and has been in business over 60 years.

Caleb Scott, an equity analyst with a large pension fund, has been asked to complete a comprehensive analysis of Delicious in order to evaluate the possibility of a future investment.

Scott compiles the selected financial data found in Exhibit 1 and learns that Delicious owns a 30% equity interest in a supplier located in the United States. Delicious uses the equity method to account for its investment in the U .S . associate.

Scott reads the Delicious's revenue recognition footnote found in Exhibit 2.

Exhibit 2: Revenue Recognition Footnote

____________________________________________________________________________

in millions___________________________________________________________________

Revenue is recognized, net of returns and allowances, when the goods are shipped to customers and collectability is assured. Several customers remit payment before delivery in order to receive additional discounts. Delicious reports these amounts as unearned revenue until the goods are shipped. Unearned revenue was 7,201 at the end of 2009 and 5,514 at the end of 2008.

Delicious operates two geographic segments: Europe and Mexico. Selected financial information for each segment is found in Exhibit 3.

At the beginning of 2009, Delicious entered into an operating lease for manufacturing equipment. At inception, the present value of the lease payments, discounted at an interest rate of 10%, was 6300 million. The lease term is six years and the annual payment is 669 million. Similar equipment owned by Delicious is depreciated using the straight-line method and no residual values are assumed.

Scott gathers the information in Exhibit 4 to determine the implied "stand-alone" value of Delicious without regard to the value of its U .S . associate.

When applying the financial analysis framework to Delicious, which of the following is the best example of an input Scott should use when establishing the purpose and context of the analysis?

The institutional guidelines related to developing the specific work product is an input source in the first phase (defining the purpose and context of the analysis). Audited financial statements are an example of an input in the data collection phase. Ratio analysis is an example of the output from the data processing phase. (Study Session 7, LOS 26.a)

Tamara Ogle, CFA, and Isaac Segovia, CAIA, are portfolio managers for Luca's Investment Management (Luca's). Ogle and Segovia both manage large institutional investment portfolios for Luca's and are researching portfolio optimization strategies.

Ogle and Segovia begin by researching the merits of active versus passive portfolio management. Ogle advocates a passive approach, pointing out that on a risk-adjusted basis, most managers cannot beat a passive index strategy. Segovia points out that there will always be a need for active portfolio managers because as prices deviate from fair value, active managers will bring prices back into equilibrium. They determine that Treynor-Black models permit active management within the context of normally efficient markets.

Ogle decides to implement Treynor-Black models in her practice and starts the implementation process. In conversations with her largest client's risk manager, Jim King, FRM, she is asked about separation theorem in relation to active portfolio management. She responds that separation theorem more properly relates to asset prices deviating from and gravitating toward their theoretical fair price. King next asks Ogle about the differences between the Sharpe ratio and the information ratio and the difference between the security market line (SML) and the capital market line (CML).

After reallocating her client portfolios based on using the Treynor-Black model, Ogle discusses the results with Segovia. Ogle states that she is satisfied with the current methodology, but given her preference for passive management, she is still concerned about relying on analyst's forecasts. Segovia tells Ogle that he will research methods for modifying the Treynor-Black model to account for analyst forecasts.

The optimal portfolio for an investor under the Treynor-Black model:

While theTrcynor-Black model can be modified to include analyst forecast accuracy in the calculation of active portfolio weights, this is not part of the model itself. The unsystematic risk of securities in the active portfolio is an important input into the information ratio and active portfolio weights. A change in the risk-free rate can be expected to change an investor's allocation between the risk-free asset and the optimal risky portfolio and will change the estimates of abnormal returns (alpha) for active portfolio stocks and, thereby, their portfolio weights. (Study Session 18, LOS 67.b)

Martha Garret, CFA, manages fixed income portfolios for Jones Brothers, Inc. (JBI). JBI has been in the portfolio management business for over 23 years and provides investors with access to actively managed equity and fixed-income portfolios. All of JBI's fixed-income portfolios are constructed using U .S . debt instruments. Garret's primary portfolio responsibilities are the Quasar Fund and the Nova Fund, both of which are long fixed-income portfolios consisting of Treasury securities in all maturity ranges. The Quasar Fund holdings as of March 15 are provided in Exhibit 1. A comparison of key rate durations for the Quasar Fund and Nova Fund is provided in Exhibit 2.

Of particular importance to Garret and her colleagues is the degree of interest rate risk exposure unique to each portfolio under JBI's management. Driving the increased awareness of the portfolios' interest rate exposure is the double digit growth in assets under management that JBI's fixed-income portfolios have experienced in the last five years. Interest in the company's fixed-income portfolios continues to grow and as a result, all portfolio managers are required to attend weekly meetings to discuss key portfolio risk factors. At the last meeting, Miranda Walsh, a principal at JBI, made the following comments:

"The variance of daily interest rate changes has been trending higher over the last three months leading us to believe that a period of high volatility is approaching in the next twelve to eighteen months. However, the reliability is questionable since the volatility estimates were derived using an option pricing model, which assumes constant interest rates."

"Also, the Treasury spot rate curve currently has a similar shape to the yield curve on Treasury coupon securities, which, according to the market segmentation theory of interest rate term structure, indicates a relatively high level of demand from investors for intermediate term securities. Overzealous trading by investors unwilling to move into other maturity ranges may create mispricing and opportunities for arbitrage."

After the meeting, Walsh and JBI's other principals met to discuss a new international portfolio opportunity. At Walsh's suggestion, the principals selected Garret as the lead portfolio manager for the new fund, which will be titled the Atlantic Fund. One of the other portfolio managers, Greg Terry, CFA, suggested to Garret that she utilize the LIBOR swap curve as a benchmark for the Atlantic fund rather than using local government yield curves. Terry justifies his suggestion by claiming that "the lack of government regulation in the swap market makes swap rates and curves directly comparable between different countries despite fewer maturity points with which to construct the curve as compared to a government yield curve. Furthermore, credit risk in the swap curves of various countries is similar, thus avoiding the complications associated with different levels of sovereign risk embedded in government yield curves.'' Intrigued by the idea of using the swap curve, Garret has her assistant begin gathering a range of current and forward LIBOR rates.

Assume that Bond A is currently callable at 105 and will be callable at 103 in six months. If the yield curve experiences a negative butterfly shift over the next month, which of the following results is most likely to be observed?

Bond A is priced at par value. A negative butterfly shift would increase the humped nature of the yield curve, either through a bigger increase in intermediate rates than short and long rates or a smaller decrease in intermediate rates than short- and long-term rates. Because Bond A has a much lower duration than Bond C, a yield curve shift would have more of a price impact on Bond C than Bond

A . Long-term investors would not be drawn to such a short-term bond unless the yield shift created significant mispricing, which is unlikely. Choice C is the only answer that accurately reflects a possible result of a negative butterfly shift. Bond A would increase in price if the shift saw short-term rates falling more than intermediate rates. The increase in price will be limited, however, by the call price and thus the callable bond would experience price compression (usually observed at low interest rates). The interest rate decrease would be consistent with a negative butterfly shift. (Study Session 14, LOS 53.a)

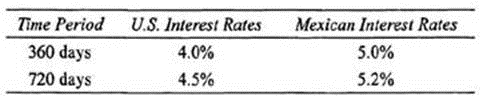

Rock Torrey, an analyst for International Retailers Incorporated (IRI), has been asked to evaluate the firm's swap transactions in general, as well as a 2-year fixed for fixed currency swap involving the U .S . dollar and the Mexican peso in particular. The dollar is Torrey's domestic currency, and the exchange rate as of June 1,2009, was $0.0893 per peso. The swap calls for annual payments and exchange of notional principal at the beginning and end of the swap term and has a notional principal of $100 million. The counterparty to the swap is GHS Bank, a large full-service bank in Mexico.

The current term structure of interest rates for both countries is given in the following table:

Torrey believes the swap will help his firm effectively mitigate its foreign currency exposure in Mexico, which sterns mainly from shopping centers in high-end resorts located along the eastern coastline. Having made this conclusion, Torrey begins writing his report for the management of IRI. In addition to the terms of the swap, Torrey includes the following information in the report:

* Implicit in the currency swap under consideration is a swap spread of 75 basis points over 2-year U .S . Treasury securities. This represents a 10 basis point narrowing of the spread as compared to this time last year. Thus, we can assume that the credit risk of the global credit market has decreased. Unfortunately, the decline provides no insight into the credit risk of the individual currency swap with GHS Bank, which could have increased.

* In order to decrease the counterparty default risk on the currency swap, we will need to utilize credit derivatives between the beginning and midpoint of the swap's life when this particular risk is at its highest. This is a significantly different strategy than we normally use with interest rate swaps. For interest rate swaps, counterparty default risk peaks at the middle of the swap's life, at which point we utilize credit derivative CQuntermeasures to offset the risk.

* Because currency swaps almost always include netting agreements and interest rate swaps can be structured to include mark-to-market agreements, we can significantly reduce the credit risk of these swap instruments by negotiating swap contracts that include these respective features. When negotiating these features is not possible, credit risk can be reduced by using off-market swaps that do not require an initial payment from IRI.

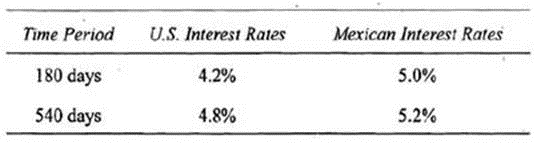

Six months have passed (180 days) since Torrey issued his report to IRI's management team, and the current exchange rate is now $0,085 per peso. The new term structure of interest rates is as follows:

Calculate the value of the 2-year currency swap from the perspective of the counterparty paying dollars six months after Torrey's initial analysis.

Use the new Mexican term structure to derive the present value factors:

Zl80 (360) - 1 / [1 4 0.050(180 / 360)] = 0.9756

Z180 (720) = 1 / [1 t 0.052(540 / 360)] = 0.9276

The present value of the fixed payments plus the principal is:

0.0507 x (0.9756 + 0.9276) + 0.9276 = 1.0241 per peso

Apply this to notional principal and convert at current exchange rate:

1.0241 x ($100M / 0.0893) m 0.085= $97.48 million

The value of the swap is the difference between this value and the pay dollar fixed present value derived in the previous question:

$97

.48 - $101.69M = - $4.21 million (Study Session 17, LOS 61 A)

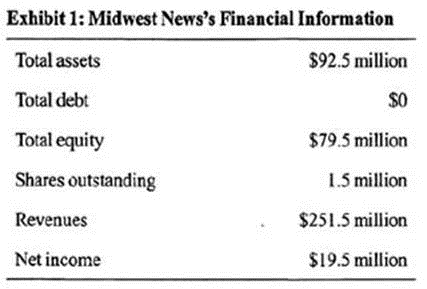

Sentinel News is a publisher of over 100 newspapers around the country, with the exception of the Midwestern states. The company's CFO, Harry Miller, has been reviewing a number of potential candidates (both public and private companies) that would provide Sentinel News entrance into the Midwestern market. Recently, the founder of Midwest News, a private newspaper company, passed away. The founder's family members are inclined to sell their 80% controlling interest. The family members are concerned that Midwest News's declining newspaper circulation is not cyclical, but rather permanent. The family members would reinvest the cash proceeds from the sale of Midwest News into a diversified portfolio of stocks and bonds. Miller's staff collects the financial information shown in Exhibit 1.

Miller noted that Midwest News does not pay a dividend, nor does the company have any debt. The most comparable publicly traded stock is Freedom Corporation. Freedom, however, has significant radio and television operations. Freedom's estimated beta is 0.90, and 40% of the company's capital structure is debt. Freedom is expected to maintain a payout ratio of 40%. Analysts are forecasting the company will earn S3.00 per share next year and grow their earnings by 6% per year. Freedom has a current market capitalization of S15 billion and 375 million shares outstanding. Freedom's current market value equals its intrinsic value.

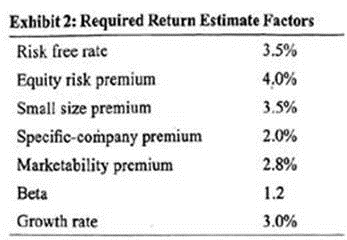

Miller's staff uses current expectations to develop the appropriate equity risk premium for Midwest News. The staff uses the Gordon growth model (GGM) to estimate Midwest's equity risk premium. The equity risk premium calculated by the staff is provided in Exhibit 2.

Miller believes the best method to estimate the required return on equity Midwest News is the build-up method. All relevant information to determine Midwest News's required relurn on equity is presented in Exhibit 2.

The specific-company premium reflects concerns about future industry performance and business risk in Midwest News. Miller makes two statements concerning the valuation methodology used to value Midwest News's equity.

Statement I: The required return estimate that is calculated from Exhibit 2 reflects all adjustments needed to make an accurate valuation of Midwest News.

Statement 2: It is better to use the free cash flow model to value Midwest News than a dividend discount model.

Miller considered two different valuation models to determine the price of Midwest News's equity: a single-stage free cash flow model and a single-stage residual income model.

Based on Exhibit 2 and using the build-up method, Midwest News's required return on equity is closest to:

= risk-free rate + equity risk premium + size premiu + specific-company premiu

Control premium and marketability premium adjustments are not usually made in the required return on equity calculation, but rather directly to the estimated value. (Study Session 10, LOS 35.d)

- Select Question Types you want

- Set your Desired Pass Percentage

- Allocate Time (Hours : Minutes)

- Create Multiple Practice tests with Limited Questions

- Customer Support

Elmira

15 hours agoCaitlin

8 days agoGerman

16 days agoViki

24 days agoFletcher

1 month agoWilliam

1 month agoHaydee

2 months agoJeffrey

2 months agoJani

2 months agoRoyce

2 months agoNadine

2 months agoEmiko

3 months agoChuck

3 months agoStanford

3 months agoDeonna

3 months agoEleni

4 months agoErick

4 months agoKizzy

4 months agoDeane

5 months agoJeannine

5 months agoSkye

5 months agoJudy

5 months agoAshleigh

5 months agoDylan

6 months agoVirgina

6 months agoPaola

6 months agoCorinne

9 months agoFelice

11 months agoNickolas

1 year agoCyndy

1 year agoJosphine

1 year agoBong

1 year agoMabel

1 year agoSanda

1 year agoDyan

1 year agoOmega

1 year agoRoy

1 year agoBillye

1 year agoSherell

1 year agoMichel

1 year agoLeslie

1 year agoLinette

1 year agoWade

1 year agoCletus

2 years agoFloyd

2 years agoGraciela

2 years agoGeorgene

2 years agoIsreal

2 years ago