Free Preparation Discussions

CFA Institute Exam CFA-Level-II Topic 1 Question 41 Discussion

Topic #: 1

Jonathan Adams, CFA, is doing some scenario analysis on forward contracts. The process involves pricing the forward contracts and then estimating their values based on likely scenarios provided by the firm's forecasting and strategy departments. The forward contracts with which Adams is most concerned are those on fixed income securities, interest rates, and currencies.

The first contract he needs to price is a 270-day forward on a $1 million Treasury bond with ten years remaining to maturity. The bond has a 5% coupon rate, has just made a coupon payment, and will make its next two coupon payments in 182 days and in 365 days. It is currently selling for 98.25. The effective annual risk-free rate is 4%. Adams is also analyzing forward rate agreements (FRAs).

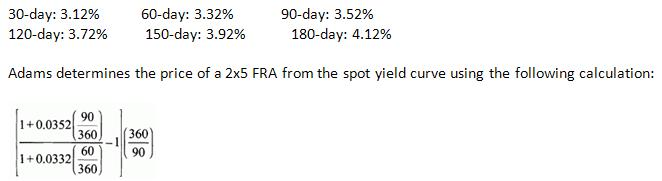

The LIBOR spot curve is as follows:

The LIBOR spot curve is as follows:

Finally, Adams wants to price and value a currency forward on euros. The euro spot rate is $1.1854. The dollar risk-free rate is 3%, and the euro risk-free rate is 4%.

How many of the following terms are correct in the calculation of the FRA price: 0.0352, 0.0332, 60/360, 90/360?

Adams used the 90-day rate (0.0352) and the time period (90/360) in the numerator instead of the 150-day rate (0.0392) and the 150-day time period (150/360). The denominator is correct, so two out of the four terms are used correctly. The correct calculation is:

(Scudy Session 16, LOS 58.c)

Currently there are no comments in this discussion, be the first to comment!