Free Preparation Discussions

CFA Institute Exam CFA-Level-II Topic 1 Question 16 Discussion

Topic #: 1

Charles Mabry manages a portfolio of equity investments heavily concentrated in the biotech industry. He just returned from an annual meeting among leading biotech analysts in San Francisco. Mabry and other industry experts agree that the latest industry volatility is a result of questionable product safety testing methodologies. While no firms in the industry have escaped the public attention brought on by the questionable safety testing, one company in particular is expected to receive further attention---Biological Instruments Corporation (BIC), one of several long biotech positions in Mabry's portfolio. Several regulatory agencies as well as public interest groups have heavily criticized the rigor of BIC's product safety testing.

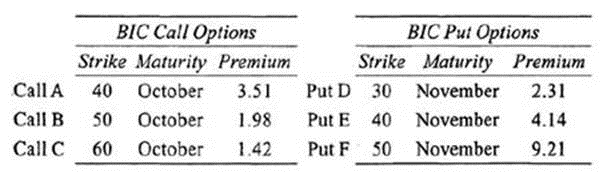

In an effort to manage the risk associated with BIC, Mabry has decided to allocate a portion of his portfolio to options on BIC's common stock. After surveying the derivatives market, Mabry has identified the following European options on BIC common stock:

Mabry wants to hedge the large BIC equity position in his portfolio, which closed yesterday (June 1) at $42 per share. Since Mabry is relatively inexperienced with utilizing derivatives in his portfolios, Mabry enlists the help of an analyst from another firm, James Grimell.

Mabry and Grimell arrange a meeting in Boston where Mabry discusses his expectations regarding the future returns of BIC's equity. Mabry expects BIC equity to make a recovery from the intense market scrutiny but wants to provide his portfolio with a hedge in case BIC has a negative surprise. Grimell makes the following suggestion:

"If you want to avoid selling the BIC position and are willing to earn only the risk-free rate of return, you should sell calls and buy puts on BIC stock with the same market premium. Alternatively, you could buy put options to manage the risk of your portfolio. I recommend waiting until the vega on the options rises, making them less attractive and cheaper to purchase."

Given Mabry's assessment of the risks associated with BIC, which option strategy would be the most effective in delta-neutral hedging the risk of BIC stock?

To protect a portfolio against an expected decrease in the value of a long equity position, put options can be purchased (i.e., a protective put strategy). The number of puts to purchase depends on the hedge ratio, which depends on the option's delta. Because the delta of the put options is negative, as the option delta moves closer to -1, the number of options necessary to maintain the hedge falls. (Study Session 17, LOS 60.e)

Currently there are no comments in this discussion, be the first to comment!