Free Preparation Discussions

AICPA CPA-Auditing Exam - Topic 3 Question 3 Discussion

Topic #: 3

When qualifying an opinion because of an insufficiency of audit evidence, an auditor should refer to the situation in the:

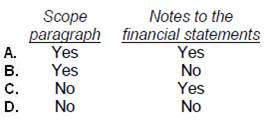

Choice "b" is correct. When a qualified opinion is issued due to a lack of sufficient audit evidence, the lack of evidence should be disclosed in an explanatory paragraph before the opinion paragraph. Since insufficient evidence is a scope limitation, the scope paragraph should also be modified to refer to the limitation and to the explanatory paragraph that discusses it.

Choices "a" and "c" are incorrect. Management (and not the auditor) prepares the notes to the financial statements. The auditor therefore would not refer to this (or any other) situation in the notes to the financial statements.

Choice "d" is incorrect. The auditor does refer to the situation in the scope paragraph.

Sena

5 months agoVanna

5 months agoJutta

5 months agoNaomi

5 months agoDoug

5 months agoReta

6 months agoRegenia

6 months agoGeoffrey

6 months agoNan

6 months ago